TL;DR:

- An intangible drilling cost (IDC) is a drilling expense with no salvage value that qualifies for immediate tax deduction. Correct classification and thorough documentation are essential to maximize benefits and avoid IRS scrutiny. Choosing between immediate expensing and amortization impacts the timing of tax deductions and future cash flow.

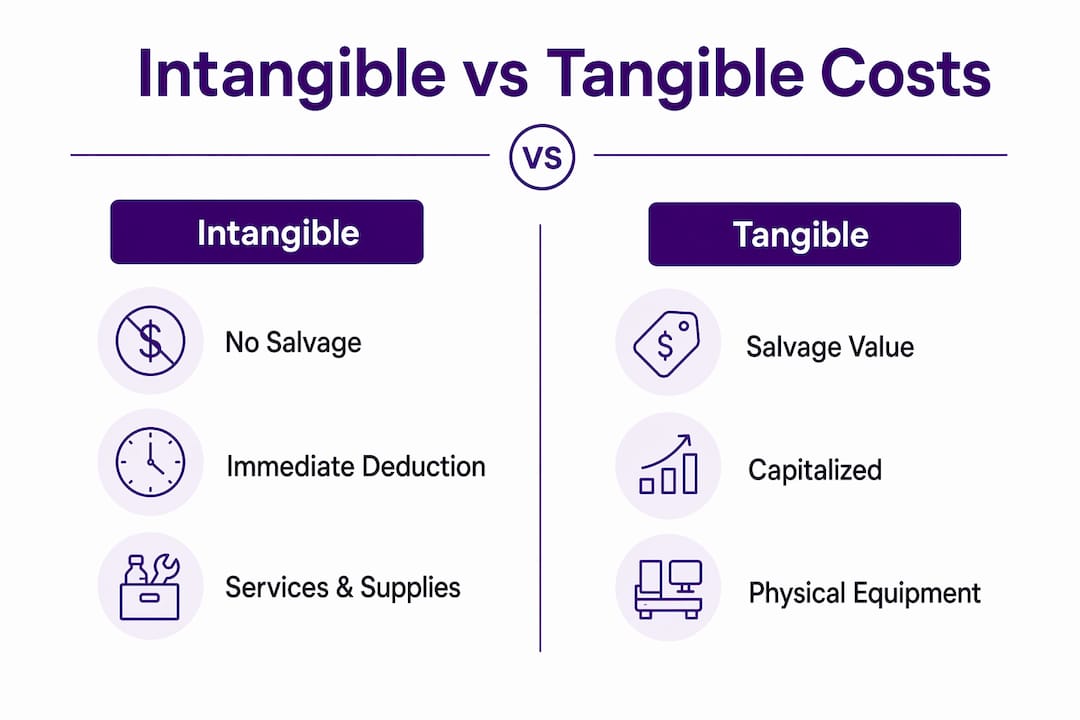

An intangible drilling cost (IDC) is defined as any drilling-related expense that has no salvage value after the well is completed, making it fully eligible for accelerated tax deduction under U.S. tax law. For accredited investors and finance professionals in oil and gas, IDCs are the primary mechanism for generating large first-year tax deductions. These costs typically represent 60% to 80% of total well expenditures, meaning on a $500,000 well, up to $375,000 may be deductible in the year the well is drilled. Understanding how IDCs are defined, classified, and reported is not optional for anyone modeling after-tax returns in energy investments.

What is intangible drilling cost and what qualifies?

Intangible drilling costs are expenses incident to and necessary for drilling and preparing oil and gas wells that produce no tangible asset with recoverable value. The IRS defines the “intangible” designation by one criterion: the expense is consumed in the drilling process and leaves nothing behind that can be sold, reused, or depreciated as physical property.

Qualifying IDC expenses include:

- Wages paid to drilling crews and rig workers during the drilling phase

- Fuel and lubricants consumed by drilling equipment

- Drilling mud and chemicals used to stabilize the wellbore

- Site preparation costs including grading and road construction to reach the drill site

- Geological surveys and seismic studies conducted before and during drilling

- Repairs to equipment during the drilling process

- Hauling and transportation of materials to the well site

- Supplies consumed during drilling operations

Every item on this list shares one characteristic: once used, it is gone. Drilling mud does not retain value after the well is completed. Wages paid to a roughneck crew cannot be recovered. This is precisely what makes these costs “intangible” in the tax sense, and it is why the IRS permits accelerated cost recovery for them.

Pro Tip: A common misconception is that any cost billed by a drilling contractor qualifies as an IDC. Contractor invoices often bundle both intangible services and tangible equipment rentals. Always request itemized billing from operators to separate IDC-eligible charges from equipment costs before filing.

How do intangible and tangible drilling costs differ?

Tangible drilling costs are expenses for physical equipment and materials that retain salvage value after drilling is complete. Wellheads, casing, tubing, pumping units, and storage tanks are all tangible. They can be removed, resold, or redeployed, which is why the IRS requires them to be capitalized and depreciated rather than immediately expensed.

The distinction matters enormously for tax timing. IDCs can be deducted in full in the year they are incurred, while tangible costs are recovered over years through depreciation schedules under the Modified Accelerated Cost Recovery System (MACRS). For a finance professional modeling investment returns, this difference in timing directly affects the net present value of the tax benefit.

| Feature | Intangible drilling costs | Tangible drilling costs |

|---|---|---|

| Nature | Services and consumed materials | Physical equipment and hardware |

| Salvage value | None | Retained; can be sold or reused |

| Tax treatment | Immediate expensing or 60-month amortization | Capitalized and depreciated (MACRS) |

| Deduction timing | Year incurred (if election made) | Over asset’s depreciable life |

| Examples | Wages, fuel, drilling mud, site prep | Casing, wellheads, pumping units |

Correct classification is not just a tax optimization exercise. Misclassifying IDC as tangible equipment costs, or vice versa, is one of the most common audit triggers in oil and gas tax returns. The IRS scrutinizes these allocations closely, and an incorrect classification can result in disallowed deductions, penalties, and interest.

What are the tax deduction options for intangible drilling costs?

The IRS provides two methods for deducting IDCs, and the choice between them is one of the most consequential elections an investor or operator makes at tax time.

Immediate expensing allows working interest owners to deduct 100% of qualifying IDCs in the tax year they are incurred. This is the default preference for most investors because it produces the largest first-year tax reduction. Working interest owners can deduct most IDCs immediately, while integrated oil companies face partial deferral and additional limitations under the tax code.

60-month amortization spreads the IDC deduction evenly over five years. This option applies when no immediate expensing election is made, or when the investor’s tax profile makes a smaller annual deduction more useful than a single large deduction. Investors with lower income in the drilling year, or those managing Alternative Minimum Tax (AMT) exposure, sometimes prefer amortization to avoid wasting deductions against income that is already sheltered.

Key considerations when choosing between the two methods:

- AMT and CAMT exposure: IDC deductions interact with the Corporate Alternative Minimum Tax (CAMT) introduced under recent legislation. Tax policy discussions continue around whether IDC deductions should be included in Adjusted Financial Statement Income (AFSI) calculations, which affects CAMT liability for corporate investors.

- Investor structure: Individual investors holding a working interest report IDCs differently than investors in partnerships or S-corporations, where deductions flow through Schedule K-1.

- Legislative environment: The One, Big, Beautiful Bill Act of 2025 introduced provisions affecting energy tax treatment. Investors should verify current IDC rules with a qualified tax advisor before filing for 2026.

- Irrevocability: The immediate expensing election, once made, cannot be reversed for that tax year. This makes pre-filing modeling critical.

Pro Tip: If you are in a high-income year with significant W-2 or capital gains income, immediate expensing of IDCs is almost always the superior choice. The deduction offsets ordinary income at your marginal rate, which for top earners means a federal tax benefit of 37 cents on every dollar of IDC deducted. Run the numbers with your CPA before the well spuds, not after.

High-earning professionals who invest in oil and gas specifically for first-year deductions should model their IDC allocation before committing capital, since the tax benefit is front-loaded and the well’s production economics play out over years.

Practical implications of IDCs for investors and finance professionals

IDCs reduce early-year taxable income significantly, which directly improves cash flow and after-tax investment returns. For a physician, attorney, or executive in the 37% federal bracket, a $300,000 IDC deduction translates to roughly $111,000 in federal tax savings in the year the well is drilled. That is capital that would otherwise go to the IRS, now retained and available for reinvestment.

Modeling IDC impact requires more than a simple percentage estimate. The investor’s holding structure matters. A direct working interest produces IDCs that flow directly to the investor’s Form 1040. A limited partnership interest produces IDCs that flow through Schedule K-1, and passive activity rules may limit how much of the deduction can offset active income. Finance professionals advising clients on oil and gas investments must account for these structural differences when projecting after-tax returns.

Audit risk is real and worth taking seriously. Proper IDC classification requires documentation at the invoice level, not just at the operator’s summary level. Investors who rely on a single-line IDC figure from an operator without reviewing underlying cost breakdowns are exposed if the IRS questions the allocation. Requesting itemized cost reports from operators before filing is a minimum standard of due diligence.

Tax policy changes continue to affect IDC treatment. Investors should monitor legislative developments, particularly around CAMT and AFSI, which could alter the effective value of IDC deductions for corporate and high-net-worth investors in future tax years. Staying current is not optional when the rules governing a core tax benefit are actively under discussion in Congress.

How to report and document intangible drilling costs for tax purposes

Accurate reporting starts with documentation. Before you can claim an IDC deduction, you need a paper trail that supports the classification of each expense as intangible rather than tangible.

Required documentation includes:

- Invoices from drilling contractors itemizing labor, fuel, supplies, and services separately from equipment charges

- Asset logs identifying any physical equipment purchased or leased during drilling

- Contracts with operators specifying the scope of drilling services and cost allocation methodology

- Operator cost reports breaking down IDC versus tangible cost allocations for the well

Reporting IDCs on your tax return depends on your ownership structure. Individual working interest owners report on Schedule C or Schedule E of Form 1040. Partnership investors receive a Schedule K-1 that passes through the IDC deduction. Form 4562 is used to report depreciation and amortization elections, including the 60-month amortization option for IDCs.

Pro Tip: The immediate expensing election for IDCs is irrevocable for the tax year in which it is made. If you file without making the election, you default to 60-month amortization and cannot go back. Confirm the election with your CPA before the return is filed, not after you receive the K-1.

Coordinating with a tax advisor who specializes in oil and gas is not a luxury. The intersection of IDC elections, passive activity rules, AMT, and CAMT creates a compliance environment where generalist CPAs routinely miss deductions or make elections that cost clients money. Doctors and executives who invest in oil and gas for tax savings consistently report that specialist tax counsel pays for itself many times over.

Key takeaways

Intangible drilling costs are the single most powerful tax deduction available to working interest owners in oil and gas, and correct classification determines whether that benefit is captured or lost.

| Point | Details |

|---|---|

| IDC definition | Drilling expenses with no salvage value, typically 60% to 80% of total well costs. |

| Qualifying expenses | Wages, fuel, drilling mud, site prep, surveys, and supplies consumed during drilling. |

| Immediate expensing | Working interest owners can deduct 100% of IDCs in the year incurred if the election is made. |

| Tangible cost contrast | Physical equipment with salvage value is capitalized and depreciated, not immediately expensed. |

| Documentation requirement | Itemized invoices, asset logs, and contracts are required to support IDC classification under IRS scrutiny. |

Why IDC strategy is more nuanced than most investors realize

From my experience working with accredited investors in oil and gas, the most common mistake is treating IDCs as a guaranteed, automatic benefit. They are not. The deduction is real and substantial, but it is conditional on correct classification, proper documentation, and the right ownership structure.

I have seen investors receive Schedule K-1s showing IDC allocations that were never verified against actual operator cost reports. When those returns were audited, the IRS reclassified a portion of the IDCs as tangible costs, triggering back taxes and penalties that wiped out a significant share of the original tax benefit. The deduction is only as good as the documentation behind it.

The legislative environment adds another layer of complexity. The ongoing debate around CAMT and AFSI treatment of IDCs is not academic. If IDC deductions are excluded from AFSI calculations for corporate minimum tax purposes, the effective value of the deduction changes for certain investor structures. Staying informed on these developments is part of managing an oil and gas position responsibly.

My honest advice: engage a CPA who works exclusively or primarily in oil and gas tax. The tax advantages for high earners in this sector are genuine and substantial, but they require active management, not passive assumption.

— Sharif

How Fieldvest helps investors maximize IDC tax benefits

Fieldvest connects accredited investors with vetted U.S. oil and gas operators who offer transparent cost breakdowns, including IDC allocations, before capital is committed. For investors who want to quantify the tax impact before writing a check, Fieldvest’s free tax deduction calculator models your first-year IDC deduction based on your income, tax bracket, and investment size.

For a broader view of how oil and gas investments reduce your tax bill across multiple strategies, the oil and gas tax guide covers IDC expensing alongside depletion allowances, passive income offsets, and structuring considerations. Both resources are built for finance professionals and high-income investors who need specifics, not generalities.

FAQ

What is an intangible drilling cost?

An intangible drilling cost is a drilling-related expense with no salvage value, such as wages, fuel, drilling mud, or site preparation, that qualifies for accelerated tax deduction under IRS rules. These costs typically represent 60% to 80% of total well expenditures.

What is the difference between intangible and tangible drilling costs?

Tangible drilling costs cover physical equipment with recoverable value, such as casing and wellheads, which must be capitalized and depreciated. Intangible drilling costs cover consumed services and materials with no residual value, which can be expensed immediately.

Can intangible drilling costs be deducted immediately?

Working interest owners can elect to deduct 100% of qualifying IDCs in the year they are incurred. Without that election, the costs are amortized over 60 months. The election is irrevocable for the tax year in which it is made.

Who is eligible to deduct intangible drilling costs?

Working interest owners in oil and gas wells are eligible for full IDC expensing. Integrated oil companies face partial limitations and deferral requirements. Passive investors who do not hold a working interest may face additional restrictions under passive activity rules.

How do intangible drilling costs affect after-tax investment returns?

IDC deductions reduce taxable income in the year the well is drilled, producing an immediate cash flow benefit equal to the deduction multiplied by the investor’s marginal tax rate. For investors in the 37% federal bracket, a $300,000 IDC deduction generates approximately $111,000 in federal tax savings in year one.

Recommended

Join our monthly energy

market Insights Newsletter