TL;DR:

- Understanding when and how deductions are triggered maximizes tax benefits for high earners.

- Proper timing, classification, and structural choices are crucial for claiming first-year energy tax deductions.

- Oil and gas IDCs offer powerful 100% first-year deductions when investment and timing are correctly managed.

Most high earners assume that picking the right investment is the hardest part of tax planning. Write a big enough check into an energy project, and the deductions follow automatically. That assumption quietly costs accredited investors thousands of dollars every year. The real leverage comes from understanding exactly when, how, and under which tax classification a deduction is triggered. First-year deductions tied to energy investments can offset enormous chunks of W2 income, but only when timing, eligibility, and structural choices line up correctly. This guide walks through every critical layer.

Table of Contents

- What are first-year tax deductions and why do they matter?

- Primary vehicles for first-year deductions in energy investments

- Tax credit interactions and stacking limits: What every high earner must know

- Case study: Oil & gas intangible drilling costs (IDCs) as a first-year deduction powerhouse

- The truth most high earners miss about first-year energy deductions

- Take the next step toward maximizing your deductions

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Understand timing rules | First-year deductions depend on when property is placed in service, not just when purchased. |

| Choose the right deduction | Section 179, bonus depreciation, and MACRS each have unique eligibility for energy investments. |

| Beware stacking limits | You can’t always combine credits and deductions—know the duplication rules to maximize benefits. |

| Leverage IDCs strategically | Intangible drilling costs in oil and gas often provide a powerful, front-loaded deduction for eligible investors. |

What are first-year tax deductions and why do they matter?

A first-year tax deduction is exactly what it sounds like: you recover the cost of an asset in the same tax year you put it to use, rather than spreading that recovery across five, seven, or fifteen years. The IRS provides several pathways to do this. First-year deductions in the U.S. are typically achieved through expensing or cost recovery rules like Section 179 and bonus depreciation, or through energy-related incentives claimed in the year property is placed in service.

For a physician earning $700,000 in W2 income or a tech executive with $1.2 million in salary and bonuses, the difference between spreading a $500,000 deduction over seven years versus taking it entirely in year one is enormous. Front-loading benefits means your capital works immediately. You get cash back through reduced tax liability right now, not in small increments over the coming decade.

The top tax deduction strategies most often used by high earners in 2026 involve stacking energy-specific incentives with these front-loaded rules. But before you can stack anything, you need to understand what each mechanism actually does.

Common misconceptions that cost investors real money:

- Assuming any energy investment automatically qualifies for bonus depreciation

- Confusing the investment date with the “placed in service” date, which actually controls eligibility

- Believing that first-year deductions and energy credits can always be claimed simultaneously on the same property

- Overlooking passive activity rules that can limit deductions for W2 professionals who don’t materially participate

- Thinking Section 179 applies to passive investment interests the same way it applies to active business property

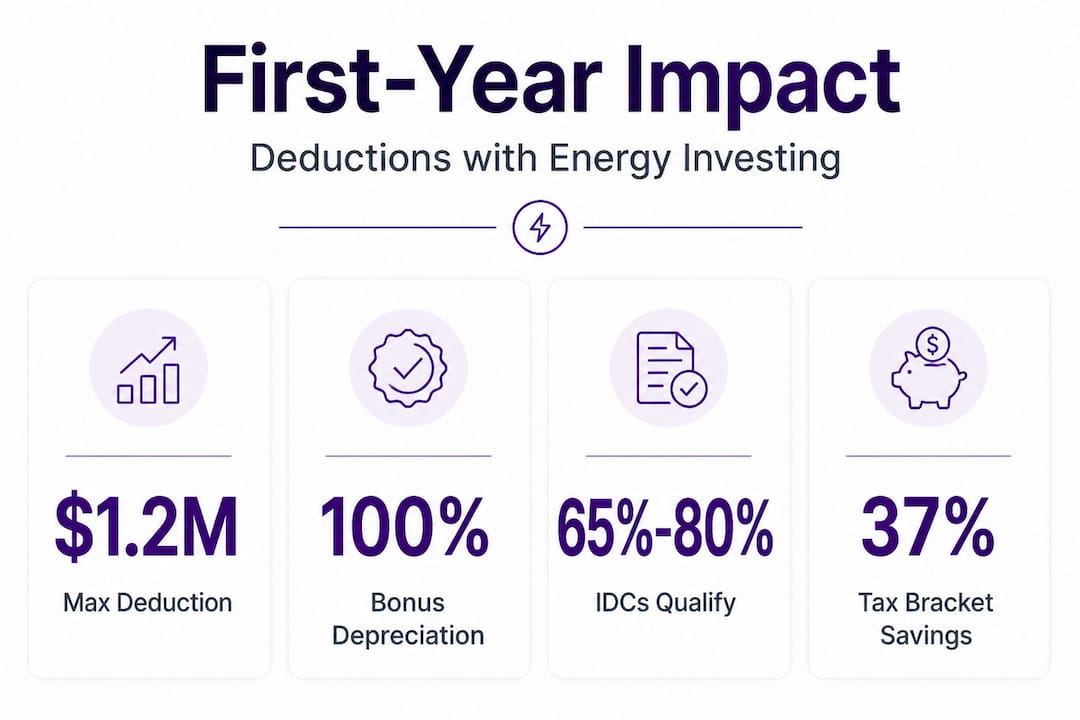

2026 update: The One Big Beautiful Bill restored and extended 100% bonus depreciation for qualified property placed in service after January 19, 2025. This is a significant reversal from the phase-down schedule that was reducing bonus depreciation by 20% per year. High earners who act in 2026 can potentially expense qualifying energy property in full during the year it’s placed in service.

Primary vehicles for first-year deductions in energy investments

Having established what first-year deductions are and why they matter, let’s look at the specific mechanisms available for energy investments. Not every vehicle works for every investor or every project structure.

The IRS recently restored 100% bonus depreciation for qualified property placed in service after January 19, 2025, reversing the annual phase-down that had been scheduled under prior law. This makes 2026 a particularly powerful year for investors who move quickly and structure deals correctly.

Clean energy property investors also benefit from accelerated cost recovery. 5-year MACRS recovery periods apply to certain qualified clean energy property placed in service after 2024, meaning even assets that don’t qualify for 100% bonus depreciation recover cost much faster than standard schedules allow.

Steps to determine which deductions your investment may qualify for:

- Identify the asset class of the property (equipment, structures, intangible costs)

- Confirm the exact “placed in service” date, not the funding or commitment date

- Check whether the property is “qualified” under Section 168(k) for bonus depreciation

- Determine whether Section 179 applies based on your active use and business classification

- Verify that your income type (active vs. passive) allows you to use the deduction in the current year

- Review any energy credit elections that may reduce your depreciable basis

| Mechanism | Max first-year benefit | Eligibility | Key limitation |

|---|---|---|---|

| Section 179 | Up to $1.22M (2026 limit) | Active business use property | Income limitation; no passive investments |

| Bonus depreciation (100%) | 100% of qualified cost | Qualified property placed in service 2025+ | Must be “qualified property” under 168(k) |

| 5-year MACRS | Accelerated over 5 years | Clean energy property post-2024 | Not immediate; spread over 5 years |

| Energy investment credit | Dollar-for-dollar credit | Qualified clean energy facilities | Reduces depreciable basis |

For investors structuring energy investments for optimal deductions, understanding when each mechanism applies prevents costly misclassification errors.

Pro Tip: You cannot always stack Section 179 and bonus depreciation on the same asset. Section 179 is applied first, and bonus depreciation then applies to any remaining basis. If you also claim an energy credit on the same property, that credit reduces your depreciable basis before either method is applied. Layer the wrong way and your effective deduction shrinks significantly.

The solar industry context matters here too. Congress has extended key solar tax credits through recent legislation, creating parallel opportunities for investors who want to blend traditional oil and gas exposure with clean energy credits.

Investors focused on direct energy investments for tax-efficient growth should recognize that the mechanism chosen shapes not just the deduction amount but also the income type offset, the year of recognition, and any basis adjustments for future sale treatment.

Tax credit interactions and stacking limits: What every high earner must know

Credits and deductions are not interchangeable. They interact in ways that frequently surprise even financially sophisticated investors.

Energy tax credits are claimed based on the “placed in service” date and carry stacking and duplication limitations that are separate from deduction rules. A credit reduces your tax owed dollar-for-dollar after your taxable income is calculated. A deduction reduces the income itself before that calculation. Both are valuable, but they interact on the same underlying asset in ways that require careful sequencing.

The “placed in service” date controls when certain benefits apply, and the cost basis for deductions must be reduced by any credits claimed. This means taking a large energy investment credit first will shrink the amount available to depreciate afterward.

| Combination | Allowed? | Effect on basis | Key form |

|---|---|---|---|

| Bonus depreciation + investment credit | Generally allowed | Credit reduces depreciable basis | Form 3468 + Form 4562 |

| Investment credit + production credit (same facility) | Not allowed | N/A | Form 3468 |

| Section 179 + bonus depreciation | Allowed (179 applied first) | Sequential, not additive | Form 4562 |

| IDC deduction + investment credit | Depends on structure | IDC basis rules separate | Operator-level documentation |

Top three stacking pitfalls and their quick fixes:

- Claiming credits before calculating adjusted basis: Always determine your credit election first, then reduce basis, then apply depreciation. Reversing this order inflates your deduction claim and creates audit risk.

- Missing the placed in service window: Investors who fund projects in December but whose property isn’t placed in service until January lose an entire tax year of benefit. Confirm operational readiness in writing before year-end.

- Assuming all energy property qualifies for the same credit rate: Post-2024 rules include bonus credit rates for projects meeting wage and apprenticeship requirements. Missing these requirements drops the credit significantly.

The IRS provides a detailed FAQ on the federal solar tax credit that illustrates how these interactions work for solar-specific investments, which is a useful parallel for understanding the broader credit-deduction relationship.

Investors reviewing oil & gas tax advantages for high earners need to understand that oil and gas operates on a different credit/deduction framework than clean energy, which is a distinction that changes the stacking analysis entirely.

Pro Tip: Use Form 3468 to formally document your energy credit election. This form also captures any basis reduction required, which feeds directly into your depreciation calculations. Completing it carelessly or after the fact creates inconsistencies that attract IRS scrutiny. Prepare it alongside your investment documentation, not as an afterthought.

The reason experienced high earners invest in oil & gas now is partly because the credit/deduction interactions in oil and gas are simpler than in clean energy, with IDCs operating largely outside the investment credit framework.

Case study: Oil & gas intangible drilling costs (IDCs) as a first-year deduction powerhouse

Intangible drilling costs represent one of the most powerful first-year deduction mechanisms available to accredited investors in the U.S. energy sector. IDCs include the costs of labor, fuel, supplies, and other expenditures necessary to drill a well that have no salvage value. They are not equipment; they are consumed in the drilling process itself.

IDCs can be deducted entirely in the first year and represent a large portion of many oil and gas project costs. In most working interest arrangements, IDCs account for 65% to 80% of total project cost in year one. For a $500,000 investment in a qualifying working interest, that means $325,000 to $400,000 could be deductible in the first tax year alone.

How investors access IDC deductions step by step:

- Invest in a qualifying working interest (not a royalty interest or limited partnership that doesn’t pass through IDCs directly)

- Confirm the operator’s classification of costs as IDCs vs. tangible equipment

- Receive a Schedule K-1 or direct documentation showing your share of IDCs

- Verify that your investment structure meets the “at-risk” rules under IRC Section 465

- Confirm that passive activity rules don’t limit your ability to use these deductions against W2 income (material participation or working interest exception typically applies)

- Claim IDCs on your individual return in the year the costs are incurred

Key statistic: In a typical domestic oil and gas project, 65% to 80% of initial project costs qualify as IDCs, all deductible in year one when properly structured.

This is why physicians and other high earners invest in oil and gas for tax savings in 2026. A physician in the 37% federal bracket who deploys $300,000 into a qualifying working interest could reduce their federal tax bill by $74,000 to $111,000 in year one from IDCs alone, before accounting for depletion allowances or production income.

Replacing a roof with solar demonstrates a similar front-loading logic for real estate owners, but the scale and speed of IDC benefits in oil and gas is difficult to match in other asset classes.

Use the oil & gas deduction calculator to model your own scenario before committing to a deal structure.

Pro Tip: Before investing, ask the operator for a written breakdown showing what percentage of projected costs are classified as IDCs versus tangible equipment. Any operator worth working with will provide this readily. If they can’t or won’t, that is a red flag about either their deal structure or their transparency.

The truth most high earners miss about first-year energy deductions

Most high earners looking at energy investments focus intensely on the size of the deduction and the credibility of the operator. Both matter. But the investors who consistently capture the largest after-tax benefits focus on a third variable that rarely gets discussed: the classification and timing precision of each cost element.

Here’s what we see repeatedly in real deals: an investor funds a project in October, the operator spends several months mobilizing, and the well doesn’t spud until February of the following year. The investor expected a current-year deduction. They get nothing until next year. Their CPA, who wasn’t looped in until tax time, has no ability to fix it retroactively.

The 11 proven tax reduction strategies for high-income earners all share a common thread: the investors who use them most effectively get advisors involved before the deal closes, not after.

“The biggest tax planning mistake high earners make isn’t choosing the wrong investment. It’s choosing the right investment at the wrong time, or without verifying the structural details that determine whether deductions actually flow through to them.”

Edge cases that catch investors off-guard: passive activity rules that prevent W2 professionals from using IDCs unless they hold a working interest directly (not through most limited partnership structures), basis reduction rules that shrink depreciation when energy credits are elected, and placed-in-service timing issues that push deductions into a future year without warning.

Checklist for verifying your investment’s eligibility:

- Written confirmation of the placed-in-service date from the operator

- Cost breakdown separating IDCs, tangible equipment, and administrative fees

- Structural documentation confirming your investment qualifies as a working interest

- At-risk basis analysis under IRC Section 465

- Passive activity analysis confirming deductions flow to your return

- CPA review of deal documents before you sign, not before you file

Pro Tip: Find a CPA who specializes in energy taxation, not just a generalist who has seen a few Schedule K-1s. The nuances of IDC classification, at-risk rules, and passive activity exceptions are detailed enough that generalist advice routinely misses significant optimization opportunities.

Take the next step toward maximizing your deductions

Understanding the mechanics is only the beginning. Putting these strategies into practice requires access to properly structured deals, vetted operators, and investments that are built to deliver the deductions they advertise.

Fieldvest connects accredited investors with trusted U.S. oil and gas operators who specialize in working interest structures that pass through IDCs and other first-year deductions directly to investors. Every deal on the platform is reviewed for structural soundness, operator track record, and tax classification clarity. If you want to see what your own deduction could look like, start with the oil & gas deduction calculator to model your scenario in minutes. When you’re ready to go deeper, Fieldvest’s platform gives you access to deals, documentation, and expert guidance designed specifically for high earners who want to lower their taxes with oil & gas investments. Your 2026 tax situation starts with the decisions you make now.

Frequently asked questions

What’s the difference between a first-year deduction and a tax credit?

First-year deductions reduce your taxable income before your tax rate is applied, while credits reduce your actual tax owed dollar-for-dollar after calculation. Energy tax credits interact with deductions differently and are not simply additive benefits on the same property.

When are energy investments eligible for first-year deductions?

Eligibility depends on when the property is placed in service, not when you invest or commit funds. Taxpayers generally must depreciate assets over multiple years unless they qualify for Section 179 or bonus depreciation elections, both of which require the placed-in-service test to be met in the target tax year.

Can I claim both an energy tax credit and a deduction on the same property?

Generally, you cannot claim both an investment credit and a production credit for the same facility, and your depreciable basis must be reduced by any credits claimed before calculating depreciation deductions.

Do IDCs really allow a 100% first-year deduction for oil and gas investments?

Yes, when the investment is properly structured as a working interest and the investor meets at-risk and passive activity rules. IDCs can be deducted entirely in the first year and typically represent 65% to 80% of a project’s initial costs.

What forms do I need to claim these first-year deductions or credits?

You’ll use IRS Form 4562 for depreciation and bonus depreciation claims. For energy credits, Form 3468 captures investment credits and the required basis reduction, which must be coordinated with your depreciation schedule.

Recommended

Join our monthly energy

market Insights Newsletter