TL;DR:

- Oil sector tax forms determine how energy investors report royalty income, working interest earnings, and partnership distributions to the IRS. Correct form selection impacts deductions, self-employment tax, and credit claims, with proper classification as passive or active income being essential. Accurate reporting of gross income and timely elections for deductions and depletion strategies help investors avoid audits and maximize tax benefits.

Oil sector tax forms are the IRS documents that determine how royalty income, working interest income, and partnership distributions get reported and taxed for investors in U.S. energy projects. This guide to oil sector tax forms covers every major form you need, from Schedule E and Schedule C to Form 1065, Schedule K-1, and Form 8904. The 2025 One Big Beautiful Bill Act made 100% bonus depreciation for qualifying intangible drilling costs permanent, which changes first-year deduction math significantly for high-income investors. Getting these forms right is the difference between a tax bill that reflects your actual liability and one that costs you thousands in missed deductions.

What is a guide to oil sector tax forms, and why does it matter?

Oil sector tax compliance requires matching each income type to the correct IRS form. The form you use is not a formality. It determines your deduction eligibility, your exposure to self-employment tax, and your ability to claim depletion.

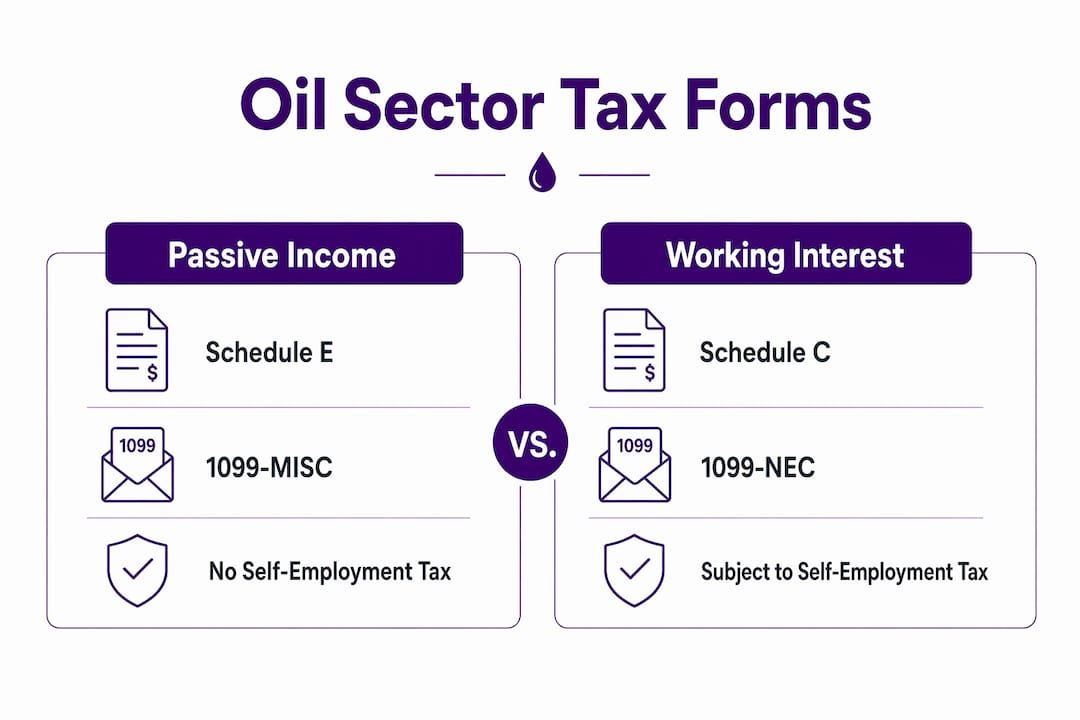

Passive royalty income for individuals goes on Schedule E, using information from Form 1099-MISC. Working interest owners report on Schedule C instead. That single distinction changes whether you owe self-employment tax on that income. Partnerships and joint ventures file Form 1065 and pass income to each partner through Schedule K-1. Investors in marginal well production use Form 8904 to claim Section 45I credits and reduce tax liability tied to low-volume wells.

Understanding which form applies to your specific investment structure is the first step in any serious oil sector tax strategy.

Which tax forms are required for different oil sector income types?

The form you file depends on how you hold your oil and gas interest. Three ownership structures drive three different reporting paths.

Passive royalty owners receive 1099-MISC from the operator and report that income on Schedule E, Part I. No self-employment tax applies. Working interest owners report on Schedule C because the IRS treats working interest income as active business income, which means self-employment tax applies on net earnings. Partnership investors receive a Schedule K-1 from the partnership’s Form 1065 filing, which breaks out their share of income, deductions, and credits.

The table below maps each income type to its primary form:

| Income type | Primary form | Key distinction |

|---|---|---|

| Passive royalty income | Schedule E + 1099-MISC | No self-employment tax |

| Working interest income | Schedule C + 1099-NEC | Self-employment tax applies |

| Partnership/JV income | Schedule K-1 from Form 1065 | Passive loss rules may apply |

| Marginal well production | Form 8904 | Section 45I credit claim |

The 1099-MISC vs. 1099-NEC distinction matters. Operators use 1099-NEC to report payments for services rendered, which signals active income to the IRS. Royalty payments go on 1099-MISC. Receiving the wrong form from an operator is a common trigger for misreporting.

Pro Tip: Request a copy of the operator’s production report each year and reconcile it against every 1099 you receive before filing. Discrepancies between the two are a leading cause of IRS inquiries.

How to report income and claim deductions on oil sector tax forms

Gross income reporting is the rule the IRS enforces most aggressively. The IRS expects gross production income on your return, not the net check you received after the operator deducted gathering, transportation, and processing costs. Investors who report only what hit their bank account routinely trigger audits.

Depletion methods: percentage vs. cost

Percentage depletion lets you deduct 15% of gross income from a property, capped at 100% of taxable income from that property. Cost depletion ties your deduction to your actual investment basis in the property. For most independent investors, percentage depletion produces a larger deduction and does not require tracking remaining basis. Large integrated oil companies are excluded from percentage depletion, so this benefit applies specifically to independent producers and royalty owners.

Intangible drilling costs and tangible drilling costs

Intangible drilling costs (IDCs) cover labor, fuel, and other non-salvageable expenses incurred drilling a well. IDCs can be expensed immediately or capitalized and amortized to avoid Alternative Minimum Tax issues under Section 59(e). Tangible drilling costs cover equipment with salvage value and are depreciated over time. The 2025 One Big Beautiful Bill Act made 100% bonus depreciation for qualifying IDCs permanent, which means a working interest owner who drills in 2026 can write off the full IDC amount in year one.

Here is the correct sequence for claiming deductions:

- Confirm your ownership classification: royalty, working interest, or partnership interest.

- Obtain gross production reports from your operator before preparing any form.

- Report gross income on the correct form (Schedule E, C, or K-1 passthrough).

- Elect your depletion method and document the calculation.

- Identify all IDCs and decide between immediate expensing and Section 59(e) amortization.

- Apply bonus depreciation to qualifying tangible costs under current law.

- Reconcile your total reported income and deductions against operator statements.

Pro Tip: Accurately identifying IDCs vs. tangible costs before filing lets you control deduction timing. Misclassifying tangible equipment as an IDC is an audit flag.

What does the step-by-step filing process look like?

A clean filing starts with document collection, not with the forms themselves. Gather every 1099-MISC, 1099-NEC, production report, royalty contract, and K-1 before opening a single IRS form. Missing one document at the start creates reconciliation problems at the end.

The core filing steps for oil investors are:

- Collect all source documents. This includes 1099s, operator production statements, lease agreements, and prior-year depreciation schedules.

- Classify each income stream. Separate royalty income, working interest income, and partnership distributions before touching any form.

- Complete Schedule E or Schedule C. Royalty owners fill out Schedule E, Part I. Working interest owners complete Schedule C with all allowable business deductions.

- Process Schedule K-1 items. Enter each K-1 line item on the correct supporting form. Box 1 ordinary income goes to Schedule E, Part II. Depletion and IDC items flow to separate deduction worksheets.

- File the Section 59(e) election if applicable. Section 59(e) allows amortizing IDCs over 60 months, which can reduce AMT exposure for high-income filers.

- Handle state severance taxes. State-level severance taxes vary by jurisdiction and are a frequent audit target. Automation tools that track state filings by asset location reduce penalty risk.

- Reconcile everything. Compare your total reported income against operator production reports line by line before submitting.

Pro Tip: Build a simple spreadsheet that maps each 1099 and K-1 to its corresponding IRS form line. This reconciliation document is your first line of defense in any IRS correspondence.

The documents you need to keep on file include:

- All 1099-MISC and 1099-NEC forms from operators

- Monthly or quarterly production statements

- Lease and royalty agreements showing your ownership percentage

- Depreciation schedules from prior years

- State severance tax filings and payment confirmations

Common challenges and tax planning strategies for high-income oil investors

High-income investors face a set of tax planning constraints that do not apply to smaller filers. The Corporate Alternative Minimum Tax can limit deductions for large entities, requiring careful coordination between depletion elections, IDC expensing, and CAMT exposure. Planning around CAMT is not optional for investors at scale.

The working interest vs. limited partnership distinction is the most consequential structural decision an oil investor makes. Working interest owners face self-employment taxes on Schedule C income, while limited partners face passive activity loss restrictions instead. Neither structure is universally better. The right choice depends on your total income picture, your passive loss carryforwards, and your deduction goals for the year.

Key planning considerations for high-income investors:

- Passive activity loss rules limit how much loss from passive investments can offset active income. Working interest income is exempt from passive activity rules, which makes it a more flexible deduction vehicle.

- Section 199A deductions may apply to qualified business income from certain oil and gas structures, but the rules are complex and structure-dependent.

- State severance tax planning requires tracking each state’s rate and filing calendar separately. Texas, Oklahoma, and North Dakota each apply different rates and exemptions.

- IDC expensing elections made in one year cannot be reversed. Get the decision right before filing.

“The classification of your oil investment as a working interest versus a limited partnership interest is not just a legal formality. It determines your entire tax reporting path, your self-employment tax exposure, and your ability to use losses against other income.”

Pro Tip: If you hold working interests in multiple states, consult a tax professional who specializes in oil and gas before filing. State severance tax rules change frequently and carry significant penalty exposure when mishandled.

Key Takeaways

Accurate oil sector tax compliance requires matching each income type to the correct IRS form, reporting gross production income, and making deliberate elections on depletion and IDC treatment before filing.

| Point | Details |

|---|---|

| Form selection drives tax outcomes | Royalty income belongs on Schedule E; working interest income belongs on Schedule C. |

| Report gross, not net | The IRS requires gross production income, not the net check received after operator deductions. |

| IDC elections are permanent | Choosing to expense or amortize IDCs under Section 59(e) cannot be reversed after filing. |

| Bonus depreciation is now permanent | The 2025 OBBBA made 100% bonus depreciation for qualifying IDCs permanent for tax years going forward. |

| Structure determines strategy | Working interest vs. limited partnership classification changes self-employment tax, passive loss rules, and deduction access. |

What I have learned from years of watching investors get this wrong

The most expensive mistake I see high-income oil investors make is treating their K-1 like a simple income statement. A Schedule K-1 from an upstream oil partnership contains depletion adjustments, IDC elections, and AMT preference items that require separate treatment on your return. Investors who hand their K-1 to a generalist CPA and assume it will be handled correctly are often disappointed at audit time.

The second pattern I see constantly is investors who wait until tax season to think about their elections. The decision to expense IDCs immediately versus amortize them under Section 59(e) has to be made with full knowledge of your projected income for the year. Making that call in april without a year-end income projection is guesswork. The investors who get the most out of oil and gas tax benefits are the ones who model their deduction scenarios in the fourth quarter, before the year closes.

The 2025 tax law changes made permanent benefits that were previously temporary. That permanence changes the planning calculus. You can now build multi-year investment strategies around 100% first-year IDC deductions with confidence. Investors who understand how to lower taxes through oil and gas structures are in a genuinely strong position right now. The tax code rewards this asset class more than almost any other for high-income filers.

— Sharif

Fieldvest connects investors with projects built for tax efficiency

High-income investors who want to put these tax advantages to work need access to vetted projects, not just knowledge of the forms. Fieldvest connects accredited investors with trusted U.S. oil and gas operators whose projects are structured to deliver large first-year deductions and long-term energy income.

Fieldvest’s free tax deduction calculator lets you model your potential first-year deduction before committing to any project. The platform focuses on projects where IDC treatment, depletion elections, and bonus depreciation are already built into the investment structure. Investors who want to see exactly how oil and gas fits their tax picture can start with Fieldvest and run the numbers before making any decision.

FAQ

What is the difference between Schedule E and Schedule C for oil income?

Schedule E reports passive royalty income with no self-employment tax. Schedule C reports working interest income, which is subject to self-employment tax because the IRS treats it as active business income.

What is Form 8904 used for in oil and gas?

Form 8904 is used to claim the Section 45I credit for oil and gas production from marginal wells. It reduces tax liability for investors with qualifying low-volume well production.

Should I expense IDCs immediately or use the Section 59(e) election?

Immediate expensing produces the largest first-year deduction but may trigger AMT issues. The Section 59(e) election amortizes IDCs over 60 months and avoids AMT preference treatment, which is often the better choice for high-income investors with significant AMT exposure.

Why does the IRS require gross income reporting for oil royalties?

The IRS requires gross production income because operators deduct gathering, transportation, and processing costs before issuing checks. Reporting only the net check understates your income and triggers audit flags when reconciled against operator production data.

How do state severance taxes affect oil sector tax compliance?

State severance taxes vary by jurisdiction and are a frequent audit target for oil and gas investors. Each state applies different rates and filing deadlines, so investors with assets in multiple states need separate tracking for each jurisdiction.

Recommended

Join our monthly energy

market Insights Newsletter