TL;DR:

- Oil and gas JVs are formal agreements with specific governance, risk sharing, and legal protections.

- Structuring ensures tax benefits, protects against operator misconduct, and influences project outcomes.

- Proper JV agreements are crucial for maximizing profit, minimizing risks, and accessing tax deductions.

Many high-income professionals assume that buying into an oil deal automatically makes them a joint venture partner. It doesn’t. The word “JV” gets thrown around loosely in energy investment circles, but the structure behind that label determines everything: your tax position, your risk exposure, your governance rights, and your ability to remove a failing operator. This guide cuts through the confusion and explains exactly what an oil and gas joint venture is, how it works legally and operationally, and why the structure itself is as valuable as the well you’re investing in.

Table of Contents

- What is a joint venture in oil and gas?

- How oil and gas JVs work: Structure, mechanics, and governance

- Tax advantages and K-1 reporting: What every investor should know

- Key risks, operator obligations, and dispute resolution

- What most guides miss: Why JV structure is investor protection (and profit) in disguise

- Next steps: Invest tax-efficiently with expert-backed JV structures

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| JV definition matters | Understanding the true meaning of ‘JV’ in oil and gas is essential for risk and tax clarity. |

| Structure drives outcomes | A well-crafted JV agreement protects your control, upside, and tax benefits. |

| Tax benefits require diligence | Maximizing deductions depends on ownership type, K-1 accuracy, and partnership mechanics. |

| Governance mitigates disputes | Clear voting rules and operator obligations in JVs reduce legal and operational risks. |

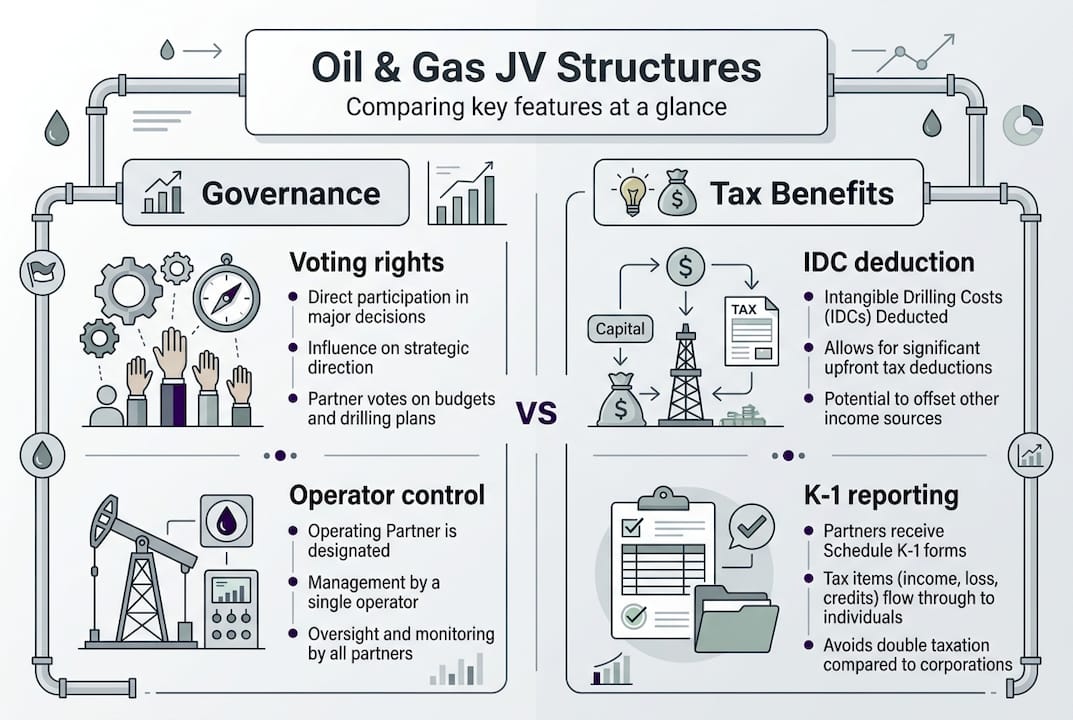

What is a joint venture in oil and gas?

A joint venture in oil and gas is a formal contractual arrangement between two or more parties to explore, develop, or produce oil and gas assets together. It’s not simply a shared investment. It’s a defined relationship with specific governance rules, cost-sharing obligations, decision-making rights, and legal protections built into the agreement.

Many investors fall into the trap of using “JV” interchangeably with other deal structures. The reality is that a JV differs meaningfully from a general partnership, a limited partnership, a working interest, or a pooled fund. Understanding the joint venturer definition helps clarify that each party in a JV retains separate legal identity while sharing project-level obligations. This is distinct from a partnership where liabilities and identities blur more significantly.

Here’s what typically defines an oil and gas JV:

- Shared ownership of a specific project or set of assets, not the companies involved

- Defined cost and revenue splits spelled out in a Joint Operating Agreement (JOA)

- Operator designation, where one party manages day-to-day operations on behalf of all parties

- Governance provisions, including voting thresholds for major decisions, budgets, and disputes

- Exit mechanisms that specify how a party can transfer or exit their interest

“Key JV/JOA mechanics that commonly matter for disputes and execution include governance, operator duties, budgeting, and default remedies.” Lexology highlights that these structural elements are what separate well-run projects from litigation-prone ones.

Capital intensity is the core reason JVs dominate oil and gas. Drilling a single well can cost anywhere from $500,000 to over $10 million depending on location and depth. No single investor wants to absorb that alone. JVs allow multiple parties to pool resources while distributing risk across participants. The structure also enables investors to access the oil and gas income streams that working interest ownership provides, including the critical tax deductions that make energy so attractive to high earners.

One common misconception: tax incentives commonly cited for working interests, such as intangible drilling cost deductions, apply based on your ownership classification, not just because you’re in a deal labeled a “JV.” The structure must be correctly set up to capture those benefits.

How oil and gas JVs work: Structure, mechanics, and governance

Once you know what a JV is, the next question is how it actually functions day to day. The answer lives almost entirely inside the Joint Operating Agreement. The JOA is the governing document that sets the rules for everything from who drills the next well to what happens when one party defaults on their cash call.

The most common JV structures in U.S. oil and gas include:

- Model Form JOA (usually AAPL Form 610): The industry standard template, widely used in domestic projects

- LLC-based JVs: Offer liability protection and pass-through taxation

- Co-tenancy arrangements: Each party holds an undivided interest in the leasehold

- Partnership structures: Typically used for multi-asset programs with multiple investors

Governance is where most investors underestimate complexity. Voting thresholds vary widely. Some JOAs require unanimous consent for capital expenditures above a set threshold, others allow an operator to proceed with a simple majority. The operator has day-to-day authority but must stay within the approved work program and budget. When disputes arise, the decision-making rules in the JOA determine who wins and how quickly the project can move forward.

Comparison: JV vs. working interest vs. pooled fund

| Feature | Joint venture (JOA) | Direct working interest | Pooled fund |

|---|---|---|---|

| Governance rights | Yes, defined in JOA | Limited or none | None (fund manager decides) |

| Liability exposure | Pro-rata, per interest | Direct and unlimited | Limited to investment |

| Tax deductions (IDC) | Yes, with proper structure | Yes, direct | Varies by fund structure |

| Operator control | Shared, with removal rights | Dependent on agreement | Fully delegated |

| Transparency | High, requires accounting | Moderate | Lower, fund-level reporting |

As blockchain-based transparency becomes more common in energy projects, JV structures are increasingly incorporating digital reporting tools, which gives non-operating investors real-time visibility into costs and production.

The most common sources of JV disputes involve budget overruns, unauthorized expenditures by the operator, and disagreements over whether to drill additional wells. A well-structured JOA addresses all of these with explicit budget approval thresholds, audit rights, and deadlock resolution procedures.

Pro Tip: Before you sign any JV agreement, make sure the JOA includes clear language on voting rights, what triggers a deadlock, and how that deadlock gets resolved. Vague language on these points has derailed more projects than poor geology ever has.

Reviewing the oil JV cash flow mechanics alongside the governance terms gives you a complete picture of what you’re actually buying into. Revenue distribution, cash call timing, and priority payout provisions all affect your real return, sometimes dramatically.

Tax advantages and K-1 reporting: What every investor should know

For high-income professionals, the tax structure of an oil and gas JV isn’t a secondary concern. It’s often the primary reason to invest. The potential to offset W-2 income or business income with large first-year deductions is a major draw, but only if the ownership structure is set up correctly.

Here’s how the main tax benefits flow through a properly structured oil and gas JV:

- Intangible drilling costs (IDCs): These cover roughly 65 to 80 percent of total drilling costs, including labor, fuel, and chemicals. For active investors with working interest status, IDCs are typically fully deductible in the year they’re incurred.

- Tangible drilling costs (TDCs): Equipment and physical assets are depreciated over time under standard MACRS schedules, providing an additional deduction stream.

- Depletion allowance: Working interest owners can deduct 15 percent of gross oil and gas income annually through the percentage depletion method, which continues even after the original cost is fully recovered.

- Operating cost deductions: Ongoing lease operating expenses are deductible each year, reducing taxable income over the life of the project.

- Passive activity rules: Investors need to understand whether their participation qualifies as active or passive, since this affects whether losses can offset non-passive income. Working interest holders in JVs often receive active status by default.

Working interest investors typically aim for deductions like IDCs and must handle proper K-1 reporting, which means your JV must be classified as a partnership for tax purposes to issue K-1s in the first place.

Major oil and gas tax deductions by ownership type

| Deduction type | JV/working interest | Royalty interest | Pooled fund/LP |

|---|---|---|---|

| IDC deduction | Full, year one | Not available | Depends on structure |

| Percentage depletion | Yes (15% of gross) | Yes (15% of gross) | Sometimes |

| Operating expenses | Yes | No | Sometimes |

| K-1 reporting | Yes | 1099 instead | Yes (at fund level) |

| Passive vs. active | Often active | Always passive | Always passive |

The K-1 reporting flow works like this. Your JV is structured as a partnership. At year-end, the partnership files Form 1065. Each partner receives a Schedule K-1 reflecting their allocable share of income, deductions, and credits. You then report these on your personal return or business entity return, depending on how you hold your interest.

Pro Tip: Keep meticulous records of your basis in the partnership from day one. Your deductible losses are limited to your at-risk basis, and the IRS scrutinizes oil and gas partnership returns carefully. Work with a CPA who specializes in energy taxation.

Use a tax savings calculator to model your potential deductions before committing capital. And if you want a fuller breakdown of how to position your income for maximum benefit, the guidance on tax savings with oil & gas JVs walks through common high-earner scenarios in detail.

Key risks, operator obligations, and dispute resolution

Every JV carries risk. The geology, the commodity price cycle, and the regulatory environment are all outside your control. But a significant class of JV risk is entirely structural, meaning it lives in the agreement itself and can be addressed before you write a check.

The most dangerous risks for a non-operating investor in an oil and gas JV include:

- Operator misconduct or negligence: An operator who cuts corners on safety, mismanages vendor relationships, or bills costs improperly can drain value fast

- Budget disputes and cash calls: Surprise cash calls beyond the approved AFE (authorization for expenditure) are a common friction point

- Deadlocks on major decisions: When partners can’t agree on whether to drill a follow-up well or abandon a location, projects stall and capital sits idle

- Default remedies that don’t protect you: If a co-venturer defaults on their cash call, the remedy provisions determine whether you’re stuck absorbing their share

Operator exculpatory clauses deserve particular attention. These are provisions in JOAs that limit operator liability to gross negligence or willful misconduct, which is a high standard to prove in court. Courts have historically enforced these clauses, so your ability to recover damages from a careless operator may be significantly limited even when you can show real losses.

“The interplay between operator duties, exculpatory clauses, and ‘shall commence’ obligations can lead to litigation and operator removal.” The Texas Crude v. Burlington Resources case illustrates how disputes over when and whether an operator must begin drilling can escalate into full removal proceedings.

Before you invest, ask your JV sponsor these critical questions:

- What are the specific grounds for removing the operator, and what vote is required?

- How are cash calls handled when one party defaults?

- What dispute escalation process is in place before litigation becomes necessary?

- Does the JOA include a deadlock mechanism, such as buy-sell or forced sale provisions?

- How are audit rights structured, and how often can non-operators request an accounting review?

Evaluating oil and gas projects properly means reading the JOA alongside the geological data and financial projections. The agreement tells you what actually happens when things go wrong. Any sponsor who resists transparency around these terms is itself a red flag.

What most guides miss: Why JV structure is investor protection (and profit) in disguise

Most explanations of oil and gas JVs stop at definitions and then move on to tax benefits. That’s useful, but it misses the deeper point: structure is outcome. Every governance clause, every voting threshold, every default remedy clause directly determines who profits, who absorbs loss, and who has power when the project hits a rough patch.

Think about it this way. Two investors put identical capital into oil and gas projects in the same basin, targeting the same formation. One enters through a loosely documented working interest arrangement. The other enters through a well-structured JOA with clear operator obligations, auditing rights, and removal provisions. When the operator underperforms, the second investor can act. The first investor is largely stuck.

The best investors in this space treat the JOA like an insurance policy. You read your insurance policy not when you’re shopping for it, but when something goes wrong. The same logic applies here. The value of strong JV structure becomes apparent the moment an operator starts missing targets, overspending budgets, or disappearing between cash calls.

Here’s the hard-won lesson from watching investors navigate this space over time: skipping the structural details costs more than picking the wrong well. A mediocre well in a well-structured JV recovers some value. A good well in a poorly structured deal can still drain you through mismanagement, disputes, or murky default provisions. The geology gets the attention, but the JOA determines the outcome.

High-income investors who treat the JV agreement as a living document, referencing it during cash call disputes or governance votes, consistently outperform those who sign and forget it. Real due diligence isn’t just about well logs and type curves. It’s about understanding whether your agreement actually protects you and whether experienced investors in similar JVs have faced these exact structural questions and come out ahead.

The contrarian truth is that a great JV structure can turn a middling energy project into a profitable one. And a weak structure can destroy the returns on an otherwise promising well. Pay attention to the paper before you pay attention to the formation.

Next steps: Invest tax-efficiently with expert-backed JV structures

Ready to put this knowledge to work? Here’s how Fieldvest can help you access expert-structured oil and gas JVs and maximize your tax benefits.

Fieldvest connects accredited investors with vetted U.S. energy operators who structure their deals with full JOA transparency, defined governance rights, and the tax mechanics that matter most to high-income professionals. Every project on the platform is reviewed for structural integrity, not just geological upside.

Start with the free oil and gas tax deduction calculator to model your first-year deduction potential based on your income and investment size. Then explore how to lower your taxes with oil and gas through properly structured working interests and JV arrangements. Fieldvest makes the complex accessible, so you invest with confidence rather than guesswork.

Frequently asked questions

How does a JV differ from a direct working interest in oil and gas?

A JV formalizes governance rights and partnership obligations under a JOA, while direct working interest is an individual ownership stake that may lack structural protections like voting rights, audit rights, or operator removal clauses.

What tax documents will I receive from a JV oil and gas investment?

Most oil and gas JVs classified as partnerships issue a Schedule K-1, which reports your allocated share of income, deductions, and credits. K-1 reporting requires strong basis tracking and correct partnership classification to ensure deductions hold up under IRS review.

What protections do JV agreements offer against partner or operator misconduct?

JV agreements include governance rules, operator performance standards, and default remedies such as dilution or removal for nonperformance. Core JV/JOA mechanics like dispute escalation procedures and operator removal clauses are your primary contractual shield against misconduct.

Are oil and gas JVs only for large institutional investors?

No. High-income professionals and accredited investors participate directly in JVs through specialized platforms and partnership structures that offer the same governance rights and tax benefits that institutional players have long relied on.

Recommended

Join our monthly energy

market Insights Newsletter